When regulators wrote the rules for cryptocurrency, they did not anticipate that Bitcoin mining facilities would become AI data centres or that crypto tokens would be used to buy and sell AI computing power or that autonomous software would execute financial transactions with no human involved. But all of this is now happening and policy frameworks are still adapting to a convergence they were not originally designed for.

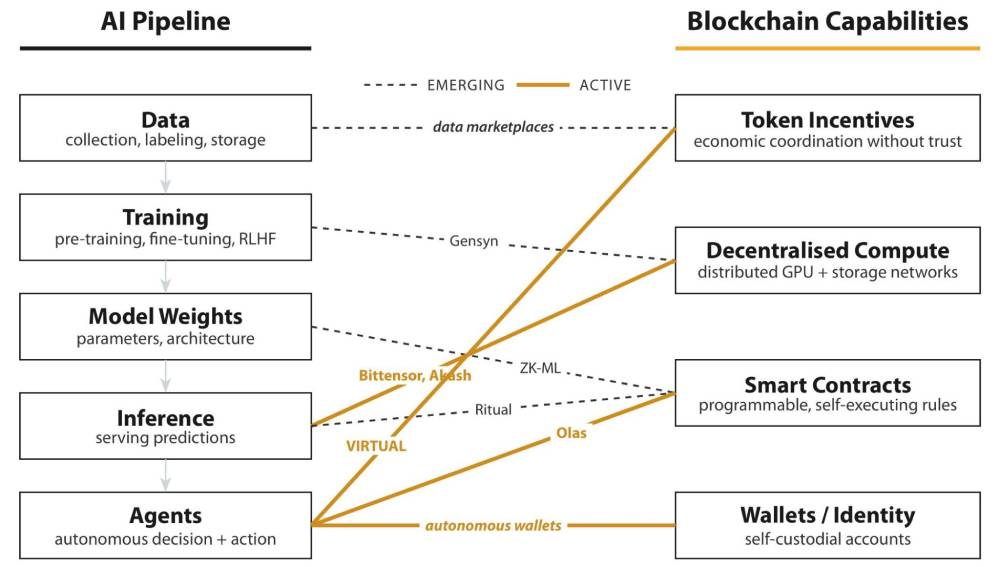

Here we trace that convergence. It begins with the physical infrastructure, where mining companies are repurposing their power and cooling systems for AI. It moves to the token economy, where a new class of crypto assets is blurring the line between payment, incentive and speculative investment. And it ends with autonomous agents, software that transacts on blockchains without anyone pressing a button. Figure 1 maps where these 2 technology stacks intersect today and where the connections are still forming.

Figure 1: Where the AI pipeline intersects with blockchain capabilities. Solid lines

indicate active integrations with deployed projects; dashed lines indicate emerging

connections.

The great mining pivot: from proof-of-work to AI compute

Bitcoin mining companies run warehouses full of specialised computers that perform proof-of-work computation, an energy-intensive process that serves as the network’s Sybil resistance mechanism, making it economically prohibitive to manipulate the transaction record and earn the block subsidy (newly minted bitcoin) for doing so. Since the April 2024 “halving,” a built-in event that cuts the block subsidy in half every 4 years, profit margins have tightened, making it harder for less efficient operators to compete. At the same time, AI hosting offers significantly higher returns per megawatt of power capacity. The result is a wave of deals in which miners lease their facilities to AI companies [1].

The pivot works because mining companies are not selling their computers. The specialised chips they use cannot run AI. What they can sell is everything around those chips: cheap electricity, grid connections that now take 3 to 5 years to obtain [2], cooling systems and physical buildings. In the simplest arrangement, AI cloud companies bring their own hardware and the miner provides a powered shell. But the business models span a spectrum: some former miners now operate their own GPU infrastructure and sell compute-as-a-service directly. IREN runs NVIDIA GPU clusters for Microsoft and Bit Digital’s WhiteFiber division hosts infrastructure for clients including Cerebras. Whether as landlord or cloud provider, the mining company leverages the same scarce resource: power, cooling and grid access.

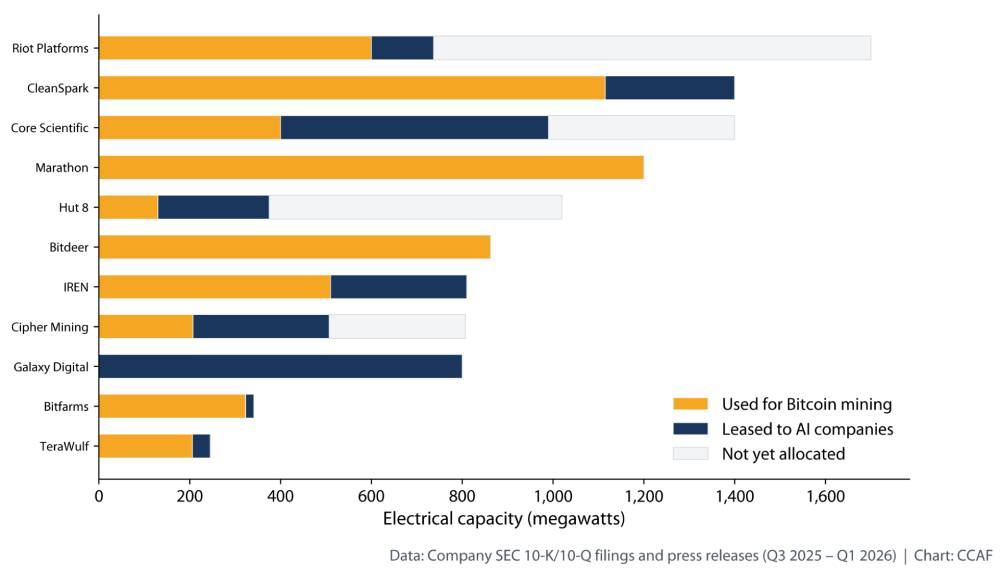

The scale of these deals reflects how valuable mining infrastructure has become to the AI industry. Cumulative announced AI and high-performance computing contract values across the publicly listed mining sector now exceed $70 billion. Hut 8 leased its River Bend campus in Louisiana for $7 billion over 15 years [3]. Core Scientific signed hosting contracts worth over $10 billion with CoreWeave [4], [5]. IREN secured a $9.7 billion AI cloud contract with Microsoft. Applied Digital committed $11 billion in capacity to CoreWeave across its Polaris Forge campus. TeraWulf’s agreements with Fluidstack, backstopped by Google, total over $12 billion in contracted revenue. Cipher Mining signed a $5.5 billion lease with AWS alongside a $3 billion hosting deal with Fluidstack. CoinShares estimates that for miners with AI contracts, mining will account for less than a fifth of revenue by late 2026 [6]. Several of the largest “Bitcoin miners” may soon earn most of their money from AI.

Several of the largest “Bitcoin miners” may soon earn most of their money from AI.

Figure 2 shows where the power is going. Across 11 publicly traded miners, roughly 2,700 MW has been committed to AI, enough to power about 2 million homes. That power could otherwise have supported 10-16% of the Bitcoin network’s total computing capacity, depending on what hardware the miners would have deployed. Bitcoin’s hashrate reached all-time highs above 1,000 EH/s in late 2025, as the difficulty adjustment mechanism attracted new, more efficient miners to replace departing capacity. But there are early signs of strain: since November 2025, the network has experienced multiple consecutive negative difficulty adjustments and the average hashrate in Q1 2026 fell roughly 8% from the Q4 2025 quarterly average, with brief peak-to-trough swings considerably larger. The causes are likely multiple (hashprice compression, hardware cycle timing and the AI reallocation itself), but the pattern warrants monitoring. As the block subsidy continues halving, the long-term question is whether transaction fee revenue alone can sustain network security. Auer [7] formalised this concern, showing that fee revenue suffers from a free-rider problem that may leave the network structurally underfunded as the subsidy declines, a prediction that the mining-to-AI reallocation now makes more pressing. This is an area the CCAF is actively investigating.

as of year-end 2025, from 10-K and 20-F filings. Contracted but not yet energised AI

capacity is excluded; including it would roughly double the AI share.

This raises several policy questions. If mining companies redirect investment toward AI, the computing power securing the Bitcoin network could decline [8]. The energy profile is changing: many miners originally operated as interruptible, demand-responsive loads, but AI data centres require firm, baseload power. Converting from one profile to the other triggers renegotiation of the interconnection agreement with the grid operator and may require updated grid impact assessments, a process that existing procedures can handle but that changes the planning assumptions under which these facilities were originally approved. The analysis here focuses on publicly listed, mostly US-based miners because they disclose capacity data through SEC filings. Bitcoin mining is a global activity, with significant operations in Kazakhstan, Russia, Ethiopia and elsewhere. The pivot dynamics almost certainly differ across jurisdictions, because the economic drivers (proximity to hyperscaler demand, access to capital markets, GPU supply chains and the regulatory environment) vary dramatically. The US concentration of AI pivot deals reflects these structural advantages, not merely a data limitation.

AI service tokens: a new asset class between utility and security

The mining pivot is about physical infrastructure. But the convergence goes deeper. A growing number of AI services are now priced, paid for and governed through crypto tokens rather than conventional subscriptions. These “AI service tokens” work as currency, incentive and investment vehicle all at once [9]. The sector remains small (aggregate market capitalisation of AI and decentralised compute tokens is roughly 1-2% of the total crypto market), but it is the fastest-growing token category and raises classification questions that existing frameworks were not designed for.

| Category | Project | Token | Token pays for | Market cap |

|---|---|---|---|---|

| Compute | Bittensor Render | TAO RENDER | AI inference, GPU time | $3.4B $900M |

| Agent | Virtuals Olas | VIRTUAL OLAS | Deploying/monetising AI agents | $500M–$800M $10M |

| Data/Marketplace | Ocean SingularityNET | OCEAN AGIX | Training data, algorithm access | Merged into ASI |

This creates a classification challenge. Regulators have made progress: the SEC and CFTC issued joint interpretive guidance in March 2026 establishing 5 token categories and classifying 16 as digital commodities [10], [11], while the EU’s MiCA regulation classifies tokens by economic substance and has been operational since late 2024 [12]. Jurisdictions with high crypto adoption, including Singapore, Nigeria and the UAE, have developed their own licensing and classification frameworks. But for multi-function AI tokens whose predominant use may shift over time (from payment to incentive to traded asset), the operational burden of monitoring and reclassification remains significant under any framework and particularly acute for regulators with smaller supervisory capacity.

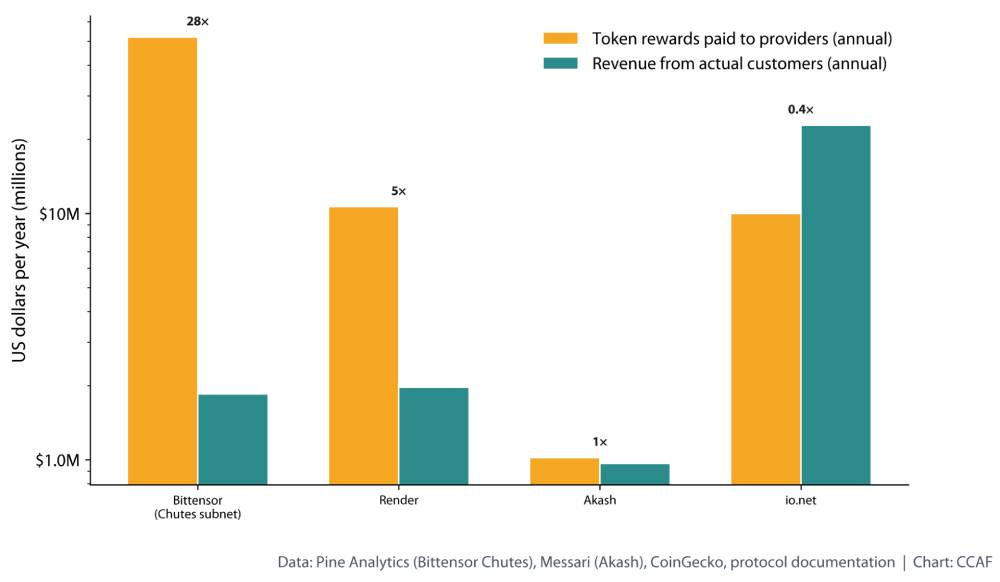

A harder question is whether these networks can survive without token incentives. Some are showing real traction: Bittensor’s network-wide revenue reached $43 million in Q1 2026 and in early 2026 over 70 independent operators collaboratively trained Covenant-72B, a 72-billion-parameter language model that matched commercially deployed open-weight models on standard benchmarks, the largest decentralised pre-training effort to date. But the economics remain subsidy-dependent. Figure 3 compares the value of token rewards paid to computing providers against actual customer revenue for 4 networks. Bittensor’s leading sub-network, Chutes, pays out 20 to 40 times more in token rewards than it earns from customers [13], a ratio that reflects early-stage growth subsidies rather than the network’s aggregate position. Render’s token emissions outpace burns, though the gap narrowed sharply in 2025 as its burn-and-mint model attracted more usage. io.net’s revenue-to-incentive ratio is narrower than Bittensor’s, though the network’s supply metrics were distorted by a 2024 attack in which fake devices flooded the system [14], [15]. Akash earned approximately $1 million in lease revenue in Q1 2025, though USD-denominated revenue fell in subsequent quarters, partly driven by a decline in AKT’s token price [16]. These are early-stage networks following a startup playbook familiar from cloud computing: AWS, Azure and GCP all subsidised early growth before achieving scale economics. Bittensor’s first halving in December 2025 cut daily TAO emissions from 7,200 to 3,600, mechanically narrowing the subsidy ratio; whether organic demand grows fast enough to fill the gap will be an early test of sustainability. Whether decentralised AI networks can follow a similar trajectory remains an open question.

networks. Bittensor figure refers to the Chutes sub-network.

Governance risks are real. The $7.5 billion merger of Fetch.ai, SingularityNET and Ocean Protocol into the Artificial Superintelligence Alliance (ASI) was completed in mid-2024 [17]. By October 2025, Ocean Protocol had pulled out, citing disputes over roughly $84 million in tokens [18]. Unlike a traditional corporate merger, there was no established legal framework to resolve the fallout.

The same token can function as a payment method, a work incentive and a tradeable asset at different points in its lifecycle. Both the US and EU frameworks now acknowledge this, but determining when a token shifts category in practice remains an open challenge.

Autonomous agents: when AI transacts without humans

The convergence goes one step further. AI software is now executing financial transactions on blockchains without per-transaction human approval. These are not simple trading bots following pre-set rules. They use language models with tool-calling capabilities and chain-of-thought reasoning to assess conditions and act autonomously, though most deployments include pre-set guardrails such as spend limits and approved action sets [19]. Most agent activity today concentrates on Ethereum and its layer-2 networks, with stablecoins (particularly USDC) serving as the dominant medium of exchange, because agents need deterministic pricing that volatile native tokens cannot provide. A recent experiment by the Bitcoin Policy Institute points in the same direction: when 36 frontier language models were given open-ended monetary decisions across 9,000 scenarios, 53% chose stablecoins for payments but 79% chose Bitcoin as a long-term store of value, a 2-tier split that emerged without any currency being suggested in the prompt [20]. Bitcoin’s scripting limitations make it less suited to the composable payment flows agents require, though Lightning Network-based protocols remain a niche area of experimentation. The potential is significant: agents that provide 24/7 market making, automate portfolio management or bring financial services to people who lack access to traditional banking.

A typical autonomous agent controls its own blockchain wallet, a kind of digital bank account. It can swap tokens, lend money or interact with blockchain-based financial services on its own. A January 2026 study catalogued the risks [21]: agents can be tricked into unintended actions, fed false data or have their cryptographic private keys extracted or misused. Once an agent sends money on a blockchain, there is no undo button. If it makes a mistake, the funds are gone.

When a company deploys an AI agent, existing regulation can assign responsibility to that company. But the harder cases are already emerging: agents deployed by anonymous developers, running on decentralised infrastructure, interacting with financial services worldwide. In those scenarios, traditional accountability frameworks struggle. TRM Labs has warned that these agents fragment responsibility across jurisdictions [22], while Chainalysis has documented the early rise of fully automated “agentic payments” [23].

The measurement gap

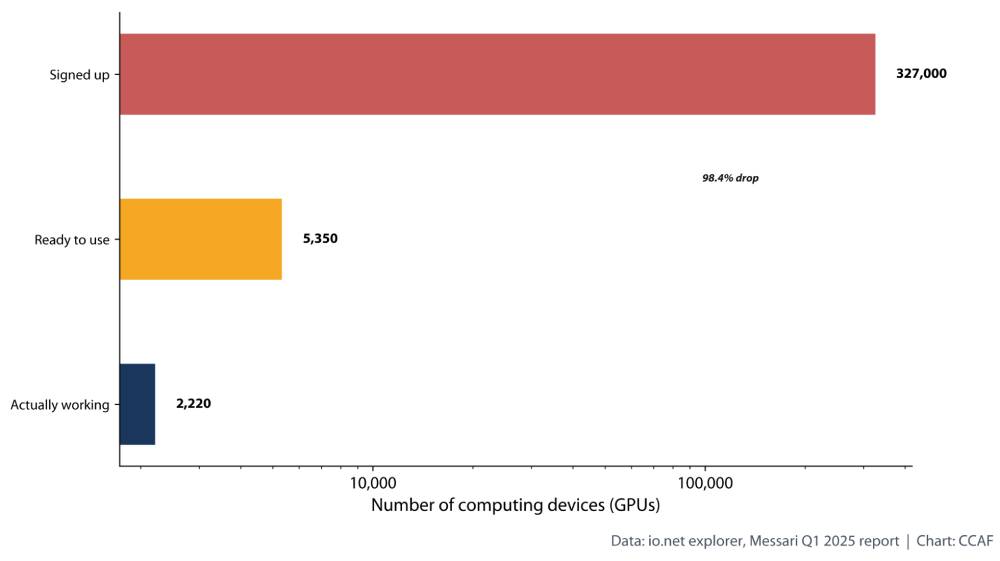

A recurring theme across all 3 layers is that the data needed to assess these developments barely exists. No public source tracks how much mining capacity has shifted to AI in aggregate. The subsidy ratios in Figure 3 required assembling data from multiple protocol dashboards and analyst reports. And the gap between claimed and actual computing capacity on distributed networks, illustrated by the io.net example in Figure 4, is something no independent body currently monitors.

This matters because policymakers are being asked to regulate a convergence they cannot yet measure. The distributed AI computing sector offers a genuine value proposition: lower costs, broader access and reduced dependence on a handful of cloud providers. In a world where GPU shortages leave many researchers and developing-country institutions locked out of AI, these networks could in principle help democratise access, though most nodes today cluster in OECD countries and latency and bandwidth constraints limit the practical benefit for users in regions with less developed internet infrastructure. But some networks’ self-reported capacity metrics have proven unreliable enough that regulators cannot easily distinguish real infrastructure from inflated claims. Independent, bottom-up measurement of both the mining pivot and decentralised AI compute is a prerequisite for sound policy.

Infrastructure dependency: the centralisation paradox

Blockchain protocols like Bitcoin and Ethereum are designed to run without any single point of control and they do: neither went down during any cloud outage in 2025. But the companies and services built on top of them are a different story. In October 2025, an AWS outage took down Coinbase, Robinhood and several other crypto platforms in minutes [24]. A similar outage in April disrupted a different set of platforms [25]. The protocols kept running; the intermediaries did not.

As blockchain-based financial services begin integrating AI, a new layer of dependency is forming. If these services rely on AI models hosted by centralised providers, an outage could disrupt the applications built on top of otherwise resilient blockchains [9]. Under the EU’s DORA regulation, the European Supervisory Authorities designated 19 critical ICT third-party providers, spanning cloud, telecom and financial technology firms, in late 2025 [26], establishing a mechanism for addressing concentration risk. Whether it should be extended to cover AI model providers is an open question. No blockchain financial protocol has yet disclosed heavy reliance on a single AI provider, but the direction of travel is clear. Distributed AI computing projects aim to reduce this dependency by spreading processing across independent nodes. But the gap between registered capacity and real usage on these networks is wide. Figure 4 illustrates the point: io.net lists 327,000 registered computing devices, a figure that includes historical registrations and devices from a 2024 period when fake sign-ups inflated the count. On a typical day, roughly 2,000 to 7,000 are active depending on the metric used [15]. Supply pools in any compute marketplace are always larger than instantaneous demand, but a gap this wide raises questions about how registered capacity figures across the sector should be interpreted.

metric.

Looking ahead, a hypothetical risk is worth flagging. As AI models become more integrated into financial services, blockchain-based financial protocols could come to depend on models hosted at facilities that were formerly mining operations. In that scenario, the same physical infrastructure would serve as both a revenue source for AI companies and a potential point of failure for the financial services built on top of it. No such dependency has been documented to date, but the general trend of AI-blockchain infrastructure convergence warrants monitoring.

What’s next

The convergence of AI and blockchain is not a future scenario. It is happening now. Regulators have begun responding: the SEC–CFTC taxonomy [10], MiCA [12], the AI Act 9 [27] and DORA [26] each address parts of the picture. But several questions cut across all of these frameworks:

How should multi-function tokens be classified in practice?

Should mining-to-AI facility conversions require new permits or updated grid impact assessments?

Who is accountable when an autonomous agent transacts?

Should AI model providers be designated as critical third parties?

DORA already covers cloud infrastructure and the ESAs’ periodic redesignation process can accommodate new systemic dependencies [26], [30]. Whether AI model providers, with their distinct risks around reliability and bias, warrant the same treatment is an open question.

None of these questions has a ready answer. But the convergence is accelerating and independent measurement of what is actually happening (how much capacity has shifted, how sustainable these networks are, how much agent activity exists) is the foundation on which sound policy must rest.

Featured authors

Wenbin Wu

Wenbin Wu is a Research Associate at the Cambridge Centre for Alternative Finance.

Acknowledgments

The author thanks Keith Bear and Alex Neumueller for helpful comments on an earlier draft.

Related articles

Finance and accounting

Integrated digital finance regulation: lessons from Kigali

Fragmentation between data protection and financial regulatory frameworks is increasing compliance burdens and slowing the development of safe, data-driven financial services. Learn what joined-up oversight would look like in practice.

Finance and accounting

Crypto privacy after sanctions – the return of coin mixers

Crypto mixers are back but different, say Wenbin Wu and Keith Bear from the Cambridge Centre for Alternative Finance (CCAF), Cambridge Judge Business School. After 2022 sanctions scattered the market, compliant privacy protocols now dominate.

AI and technology

How can AI in finance realise its full potential?

Kieran Garvey, AI Research Lead at the Cambridge Centre for Alternative Finance (CCAF), and Bryan Zhang, Co-Founder and Executive Director of CCAF, explore why banks struggle to turn AI efficiency into growth.

References

[1] Cointelegraph, “Bitcoin Mining 2026: AI Pivot, Profitability Pressure & Consolidation.” [Online]. Available: https://cointelegraph.com/news/bitcoin-mining-outlook-2026-ai-profitability-consolidation

[2] J. Rand et al., “Queued Up: 2024 Edition, Characteristics of Power Plants Seeking Transmission Interconnection As of the End of 2023,” 2024. [Online]. Available: https://emp.lbl.gov/queues

[3] C. Credits, “Hut 8 Pivots From Bitcoin to AI With $7B Google-Backed Deal to Power Data Centers.” [Online]. Available: https://carboncredits.com/hut-8-pivots-from-bitcoin-to-ai-with-7b-google-backed-deal-to-power-data-centers/

[4] The Block, “Bitcoin Miner Core Scientific to Sell Bulk of BTC Holdings in 2026 to Fund AI Pivot.” [Online]. Available: https://www.theblock.co/post/391967/bitcoin-miner-core-scientific-to-sell-bulk-of-btc-holdings-in-2026-to-fund-ai-pivot

[5] CoreWeave, “CoreWeave to Acquire Core Scientific.” [Online]. Available: https://investors.coreweave.com/news/news-details/2025/CoreWeave-to-Acquire-Core-Scientific/default.aspx

[6] CoinShares, “CoinShares Bitcoin Mining Report Q4 2025.” [Online]. Available: https://researchblog.coinshares.com/coinshares-bitcoin-mining-report-q4-2025-6ec054d71554

[7] R. Auer, “Beyond the Doomsday Economics of “Proof-of-Work” in Cryptocurrencies,” BIS Working Papers 765, 2019. [Online]. Available: https://www.bis.org/publ/work765.htm

[8] B. Magazine, “Public Bitcoin Miners Are Dumping Bitcoin For AI, A Historic Mistake.” [Online]. Available: https://bitcoinmagazine.com/business/public-bitcoin-miners-are-dumping-bitcoin-for-ai-a-historic-mistake

[9] CoinDesk, “How Decentralized AI Is Leveling the Playing Field.” [Online]. Available: https://www.coindesk.com/opinion/2026/02/22/how-decentralized-ai-is-leveling-the-playing-field

[10] U.S. Securities and Exchange Commission and Commodity Futures Trading Commission, “SEC Clarifies the Application of Federal Securities Laws to Crypto Assets.” [Online]. Available: https://www.sec.gov/newsroom/press-releases/2026-30-sec-clarifies-application-federal-securities-laws-crypto-assets

[11] Sidley Austin, “SEC Releases Landmark Interpretation on Application of U.S. Securities Laws to Crypto Assets in Coordination with CFTC.” [Online]. Available: https://datamatters.sidley.com/2026/03/24/11sec-releases-landmark-interpretation-on-application-of-u-s-securities-laws-to-crypto-assets-in-coordination-with-cftc/

[12] European Parliament, “Regulation (EU) 2023/1114 – Markets in Crypto-Assets (MiCA).” [Online]. Available: https://eur-lex.europa.eu/eli/reg/2023/1114/oj

[13] Pine Analytics, “The Bear Case for Bittensor (TAO).” [Online]. Available: https://pineanalytics.substack.com/p/the-bear-case-for-bittensor-tao

[14] io.net, “25th April Incident Report.” [Online]. Available: https://ionet.medium.com/25th-april-incident-report-176e5fb5c576

[15] Messari, “State of io.net Q1 2025.” [Online]. Available: https://messari.io/report/state-of-io-net-q1-2025

[16] Messari, “State of Akash Q3 2025.” [Online]. Available: https://messari.io/report/state-of-akash-q3-2025

[17] Y. Finance, “Ocean vs. Fetch.ai Turns Ugly: Inside the $84M ASI Token Scandal Tearing Crypto’s AI Giants Apart.” [Online]. Available: https://finance.yahoo.com/news/ocean-vs-fetch-ai-turns-212508484.html

[18] The Block, “Ocean Protocol Withdraws From AI Token Alliance With Fetch.ai and SingularityNET.” [Online]. Available: https://www.theblock.co/post/373977/ocean-protocol-withdraws-from-artificial-superintelligence-alliance

[19] Crypto.com Research, “The Rise of the Autonomous Wallet.” [Online]. Available: https://crypto.com/us/research/rise-of-autonomous-wallet-feb-2026

[20] L. Danielian, C. Brown, K. Egan, and D. Zell, “Which Money Do AI Agents Prefer?.” [Online]. Available: https://www.moneyforai.org/

[21] S. Alqithami, “Autonomous Agents on Blockchains: Standards, Execution Models, and Trust Boundaries,” arXiv preprint, 2026, [Online]. Available: https://arxiv.org/abs/2601.04583

[22] TRM Labs, “Autonomous AI Agents and Financial Crime: Risk, Responsibility, and Accountability.” [Online]. Available: https://www.trmlabs.com/resources/blog/autonomous-ai-agents-and-financial-crime-risk-responsibility-and-accountability

[23] Chainalysis, “The Convergence of AI and Cryptocurrency.” [Online]. Available: https://www.chainalysis.com/blog/ai-and-crypto-agentic-payments/

[24] CoinDesk, “The Protocol: AWS Outage Halts Some Crypto Apps.” [Online]. Available: https://www.coindesk.com/tech/2025/10/22/the-protocol-aws-outage-halts-some-crypto-apps

[25] Fortune, “Binance Among Crypto Exchanges Hit by Amazon Web Services Outage.” [Online]. Available: https://fortune.com/crypto/2025/04/15/binance-crypto-exchanges-amazon-web-services-aws-outage/

[26] European Supervisory Authorities, “The European Supervisory Authorities Designate Critical ICT Third-Party Providers Under the Digital Operational Resilience Act.” [Online]. Available: https://www.esma.europa.eu/press-news/esma-news/european-supervisory-authorities-designate-critical-ict-third-party-providers

[27] European Parliament, “Regulation (EU) 2024/1689 – Artificial Intelligence Act.” [Online]. Available: https://eur-lex.europa.eu/eli/reg/2024/1689/oj

[28] Utility Dive, “PJM Proposes Behind-the-Meter Reforms in Data Center Colocation Effort.” [Online]. Available: https://www.utilitydive.com/news/pjm-ferc-behind-the-meter-data-center-colocation/812939/

[29] The White House, “Executive Order on Accelerating Federal Permitting of Data Center Infrastructure.” [Online]. Available: https://www.whitehouse.gov/presidential-actions/2025/07/accelerating-federal-permitting-of-data-center-infrastructure/

[30] Moody’s, “Digital Economy 2026 Executive Summaries: Artificial Intelligence, Digital Finance, Cyber Risk, and Data Centers.” [Online]. Available: https://www.moodys.com/web/en/us/insights/credit-risk/outlooks/artificial-intelligence-2026.html