For decades, machine learning (ML) has increasingly powered financial services, refining risk models, fraud detection, and credit scoring. More recently, generative AI (GenAI) is enabling prompt-driven creation of coherent text, images, video, and audio while synthesising and summarising large volumes of information. Yet, as impressive as these technologies are, they have a fundamental limitation: they rely on explicit human prompts. In other words, they don’t autonomously plan or take action – they react.

Agentic AI changes that equation. Unlike GenAI, which passively responds to requests, agentic AI not only generates content but also perceives, learns and takes action via integration with tools with minimal human involvement based on set goals, enabling continuous adaptation and decision-making. Agentic AI orchestrates multiple agents using large language models as a collective brain to solve complex, multi-step problems autonomously. While still in its infancy, with poor performance and reliability to date, the technology is fast evolving with the introduction of early agentic tools such as OpenAI’s Operator and Deepmind’s Project Mariner and Anthropic’s Computer Use. Enabled by ever increasing computational power, alongside advances in model efficiency (see DeepSeek), it is likely that agentic AI’s capabilities in enhancing decision-making, automating workflows, and personalising customer interactions will soon reach a tipping point that will impact banking and financial services in profound ways.

The disruption of white-collar workflows

The first set of sectors in financial services perhaps to feel the substantial impact of Agentic AI are likely to be consulting, accounting, and auditing – professional services that have historically depended on armies of analysts and associates. Consulting firms, built on a labour-intensive, research-heavy business model, are particularly vulnerable. Agentic tools, such as the recently launched Deep Research by OpenAI, can already autonomously gather and interpret massive datasets, reason independently, highlight key trends and generate draft reports with empirical data and insights.

Auditing is another area ripe for transformation. Instead of manual transaction reviews, Agentic workflows can autonomously scan financial statements, cross-check them with compliance regulations, and flag anomalies instantly. This won’t eliminate auditors, but it will redefine their roles. Instead of focusing on routine checks, professionals will need to provide robust oversight and higher-value strategic insights – augmented by AI rather than bogged down by manual labour.

From chatbots to intelligent advisors

AI chatbots and robo-advisors are already commonplace. Agentic AI promises to take them from scripted LLM-enabled Q&A bots to intelligent assistants that can execute workflows in response to customer needs. Imagine a virtual banking agent that doesn’t just answer your queries but anticipates and acts upon your needs. If you have an outstanding credit card balance, for example, it could detect surplus funds in your savings account and suggest an optimal payment strategy – executing the transfer automatically with your approval depending on your consent thresholds.

The key is personalisation. Agentic AI will transform customer interactions by drawing on data permission capabilities enabled by open banking and embedded finance to create personalised AI agents that manage finances, optimise decisions, and align to an individual’s specific habits, goals, and risk appetite. This isn’t just about convenience – it’s about enabling everyday consumers to make smarter and more intuitive financial decisions.

The evolution of credit decisioning

Traditional credit scoring models rely on static data, providing a snapshot of risk at a single moment. The adoption of agentic AI can empower banks as well as fintechs to undertake continuous credit assessment by incorporating real-time transaction data, behavioural trends and economic indicators. The result? Faster approvals, more precise risk assessment and dynamic lending models that could adjust in real time.

But with innovation comes responsibility. Agentic AI-enabled credit decisioning raises well-documented, critical questions about bias, fairness, and accountability. If historical data reflects past discrimination, these biases could be perpetuated at scale and exacerbated by AI agents which are operating with autonomy and have their own agency. Financial institutions and regulators must carefully balance AI’s transformative power with transparency and ethical oversight to ensure fair outcomes for all borrowers. There is an important trade-off here as higher levels of explainability generally limit AI performance.

Trading and investment: a double-edged sword

Agentic AI is poised to reshape trading and investment by democratising sophisticated strategies and making advanced and autonomous trading capabilities underpinned by real-time data from APIs, sensors and social media readily accessible. Institutional investors have long relied on algorithmic trading, but Agentic AI could bring similar capabilities to retail investors, allowing for real-time portfolio adjustments, automated risk management, and intelligent investment strategies – all without human intervention.

However, this level of autonomy introduces risks. By lowering the barrier to entry, AI-driven investment agents may react to the same market signals simultaneously, it could lead to herding behaviour at scale, increasing volatility, flash crashes, or market distortions. Financial institutions and regulators will need to ensure that safeguards – such as algorithmic stress tests and additional circuit breakers – are in place to mitigate these risks before they spiral out of control.

Walking the tightrope: innovation vs governance

The promise of agentic AI in finance is enormous, but so are the challenges. Used wisely, agentic AI can widen access to financial services, reduce inefficiencies, and create hyper-personalised customer experiences. However, overreliance on AI-driven decision-making without robust oversight could undermine trust, introduce new risks, amplify biases, exacerbate discrimination and create volatility and systemic instability in financial markets.

AI-driven autonomy in financial services is no longer a futuristic concept – it’s happening now. The sustainable path forward requires investments not only in the adoption of agentic AI, but also in creating high performance explainability frameworks, algorithmic accountability and rigorous governance models. It is also imperative to think about and indeed debate the wider socio-economic and public policy implications for massive adoption of AI Agents in our financial services and economies, from job displacements, taxation regime and social welfare. One thing is certain, the agentic AI era of financial services is here and the time to act is now.

Featured authors

Bryan Zheng Zhang

Co-Founder and Executive Director, Cambridge Centre for Alternative Finance

Kieran Garvey

AI Research Lead, Cambridge Centre for Alternative Finance

Related content

A version of this article was published in this Bracken column on 25th February in The Banker, a part of the Financial Times.

Related articles in this series

Read more articles from the CCAF Perspectives series.

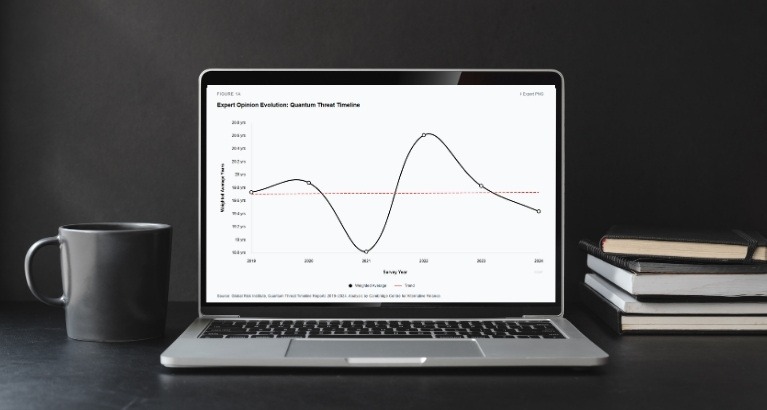

Industry leaders face a choice: act now or risk the integrity of blockchain-based markets and digital currencies, says Wenbin Wu, Research Associate at the Cambridge Centre for Alternative Finance (CCAF), Cambridge Judge Business School. Here we reveal regulators’ and policymakers’ bridging roles for quantum-resilient blockchains, and the importance of collaboration by technologists, economists, and regulators in the quantum age of financial technology.

AI and technology

How can AI in finance realise its full potential?

Kieran Garvey, AI Research Lead at the Cambridge Centre for Alternative Finance (CCAF), and Bryan Zhang, Co-Founder and Executive Director of CCAF, explore why banks struggle to turn AI efficiency into growth.

AI and technology

Innovation to impact: technology, governance and regulation

As governments worldwide grapple with the accelerating pace of technological change, the central challenge is no longer technical but institutional: how to translate digital innovation into citizen-first outcomes at scale. The obstacles lie in execution – requiring effective governance, adaptive regulation, and institutional transformation. In this piece, Carlos Montes (Lead – Cambridge Innovation Hub for Prosperity), Montek Singh Ahluwalia (citizen-first public servant and economic reformer), and Pavle Avramovic (Head of Market and Infrastructure Observatory at the CCAF), examine how public institutions can move from policy ambition to real-world impact by building innovation-ready systems that prioritise citizens over processes